June 2025 Index Returns

In stocks (equities):

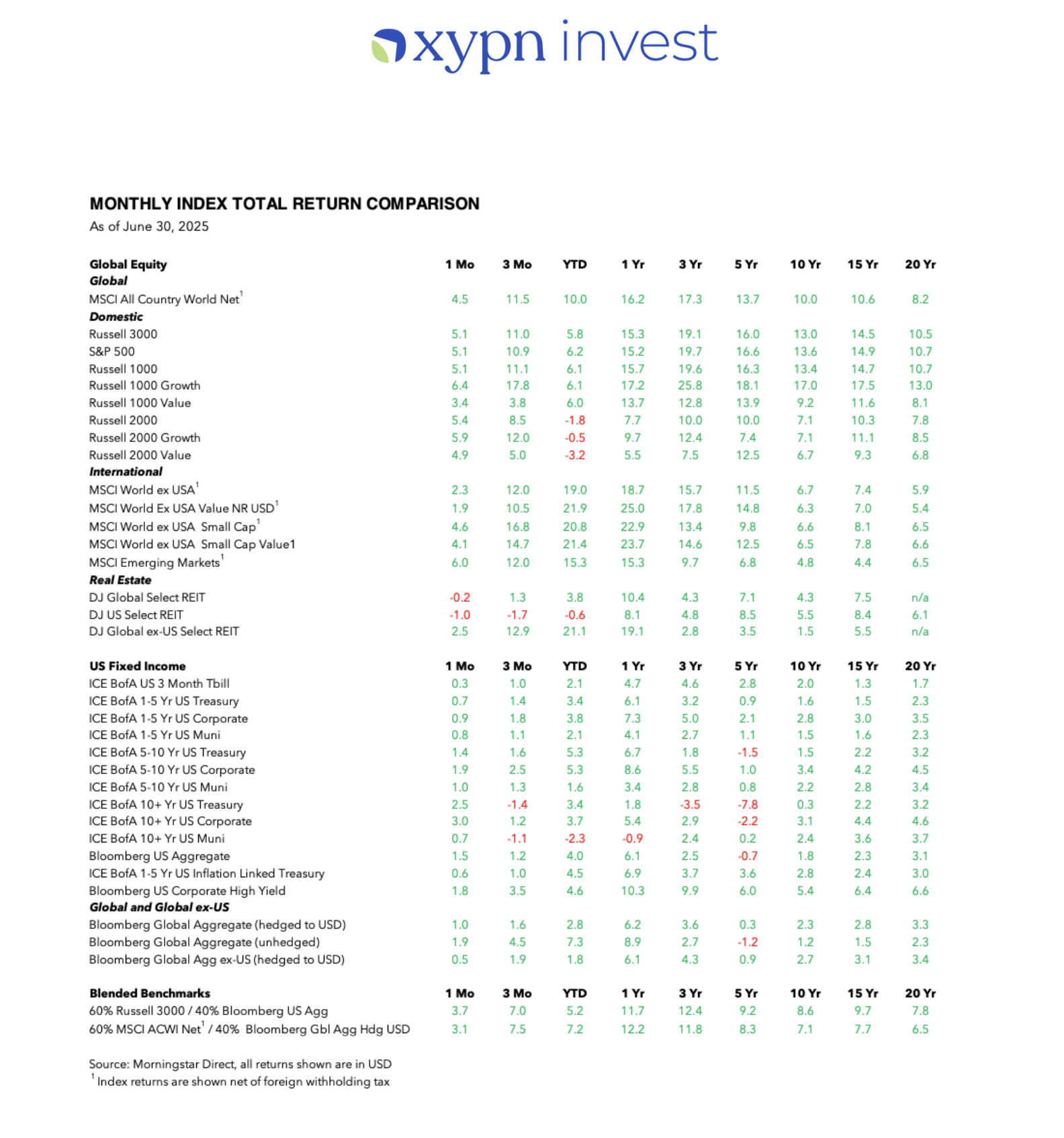

- June was another productive month for the S&P 500 Index (+5.1%) as it hit another all-time high to end the month even with trade talks between the U.S. and some of its major trading partners still ongoing and providing little detail. In addition, the U.S. Senate is in the midst of a marathon session with aims to pass President Trump's tax and spending bill with further changes and amendments still possible. Each of these situations provide enough ambiguity alone but together set an uncertain backdrop for markets.

- In the U.S., all market caps and style segments of stock markets were up in June as the Russell 3000 Index rose +5.1% with large-cap growth stocks represented by the Russell 1000 Growth Index rising the most at +6.4%. On a YTD basis, large-cap growth stocks are now back in positive territory (+6.1%) and are slightly outpacing large-cap value stocks (+6.0%) as measured by the Russell 1000 Value Index. U.S. small-cap stocks, as measured by the Russell 2000 Index, are lagging the market so far on a YTD basis (-1.8%) but beat the overall U.S. market in June by returning +5.4%.

- Internationally, stocks have continued their upward trend to start the year with developed markets measured by the MSCI World ex USA Index up +2.3% last month and emerging markets up +6.0% as measured by the MSCI Emerging Markets Index during the same period.

- On a YTD basis, global stock markets are up +10.0% (MSCI All Country World Net Index), which continue to be driven primarily by stock markets outside of the U.S.. International developed large-cap value stocks, as measured by the MSCI World ex USA Value Index, have posted the largest YTD gain (+21.9%) of all global market segments and are outpacing the S&P 500 by 15.7% so far this year. International small cap value stocks (MSCI World ex-USA Small Cap Value) have gained 21.4% YTD.

In fixed income (bonds):

- Bond returns in Treasuries were positive for all maturities this month as yields fell on average across the yield curve with market participants now expecting three interest rate cuts by the Federal Reserve between now and year's end according to CME FedWatch.

- Corporate and municipal bonds were positive across all maturity segments. The Bloomberg U.S. Aggregate Bond Index was up +1.5% last month.

- Outside of the U.S., the Bloomberg Global Agg ex-US (hedged to USD) Index was up +0.5% last month.

- All bond segments continued to show positive performance over the trailing one and three year periods with the exception of long-dated muni's one-year performance and long-dated U.S. treasuries' three-year performance.

Even with continued volatility in the U.S. stock market and heightened geopolitical uncertainty around the world, a globally balanced 60/40 portfolio is now up +7.2% YTD, which reinforces the benefits of a well-diversified portfolio and that we must focus only on what we can control.

- As always, please let us know if you have any questions by emailing support@xyinvestmentsolutions.com

- As an additional note, please keep in mind that these reflect historical performance of the current models, not necessarily how accounts were invested in the past.