July 2025 Index Returns

In stocks (equities):

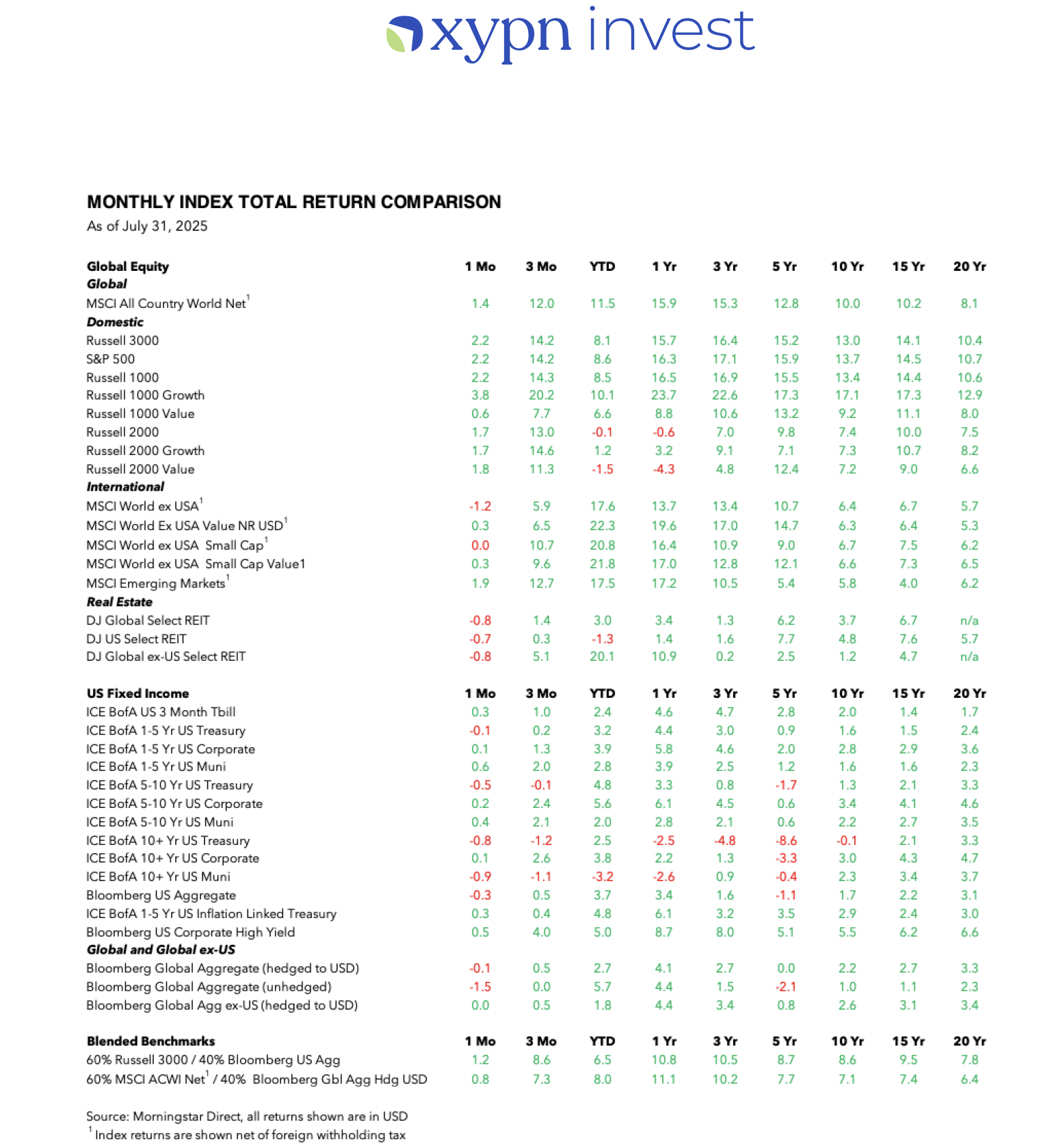

- July marks the third consecutive month this year in which the S&P 500 index (up 2.2% in July) set a record high.

- The U.S. stock market remained resilient overall in the face of tariffs and unfolding trade negotiations with the Russell 3000 index returning +2.2% for the month. Large-cap growth stocks have had a strong start to begin Q3 with the Russell 1000 growth index (+3.8%) leading the U.S. market. Their small-cap value stock counterparts as measured by the Russell 2000 Value index fell slightly behind the U.S. market last month (+1.8%) and remain down on the year (-1.5%).

- International developed stock markets as measured by the MSCI World ex USA index posted only their second monthly decline (-1.2%) of the year in July. However small-cap value stocks in global ex-U.S. developed markets were slightly positive for the month as represented by the MSCI World ex USA Small Cap Value index (+0.3%). Emerging market stocks rose +1.9% during the month as represented by the MSCI Emerging Markets index.

- On a YTD basis, the highest performing stock benchmark was international large-cap value, which gained +22.3% and has outpaced U.S. large-cap growth stocks (Russell 1000 Growth index) by +12.2% so far.

In fixed income (bonds):

- The latest Fed decision by the Federal Open Market Committee (FOMC) left short-term rates unchanged last month. Bond returns in Treasuries were negative for all maturities this month, with the exception of ultrashort maturities, as yields rose across the yield curve with market participants ending the month expecting only one interest rate cut by the Federal Reserve in one of it's last three meetings between now and year's end according to CME FedWatch.

- Corporate and municipal bonds were positive across all short-to-intermediate maturity segments while longer-dated municipal maturities saw yields increase. The Bloomberg U.S. Aggregate Bond Index was down -0.3% last month.

- Outside of the U.S., the Bloomberg Global Agg ex-US (hedged to USD) Index was flat last month.

- All bond segments continued to show positive performance over the trailing one and three year periods with the exception of long-dated municipals and treasuries.

Even with continued volatility in the U.S. stock market and heightened geopolitical uncertainty around the world, a globally balanced 60/40 portfolio is now up +8.0% YTD, which reinforces the benefits of a well-diversified portfolio and that we must focus only on what we can control.

- As always, please let us know if you have any questions by emailing support@xyinvestmentsolutions.com

- As an additional note, please keep in mind that these reflect historical performance of the current models, not necessarily how accounts were invested in the past.