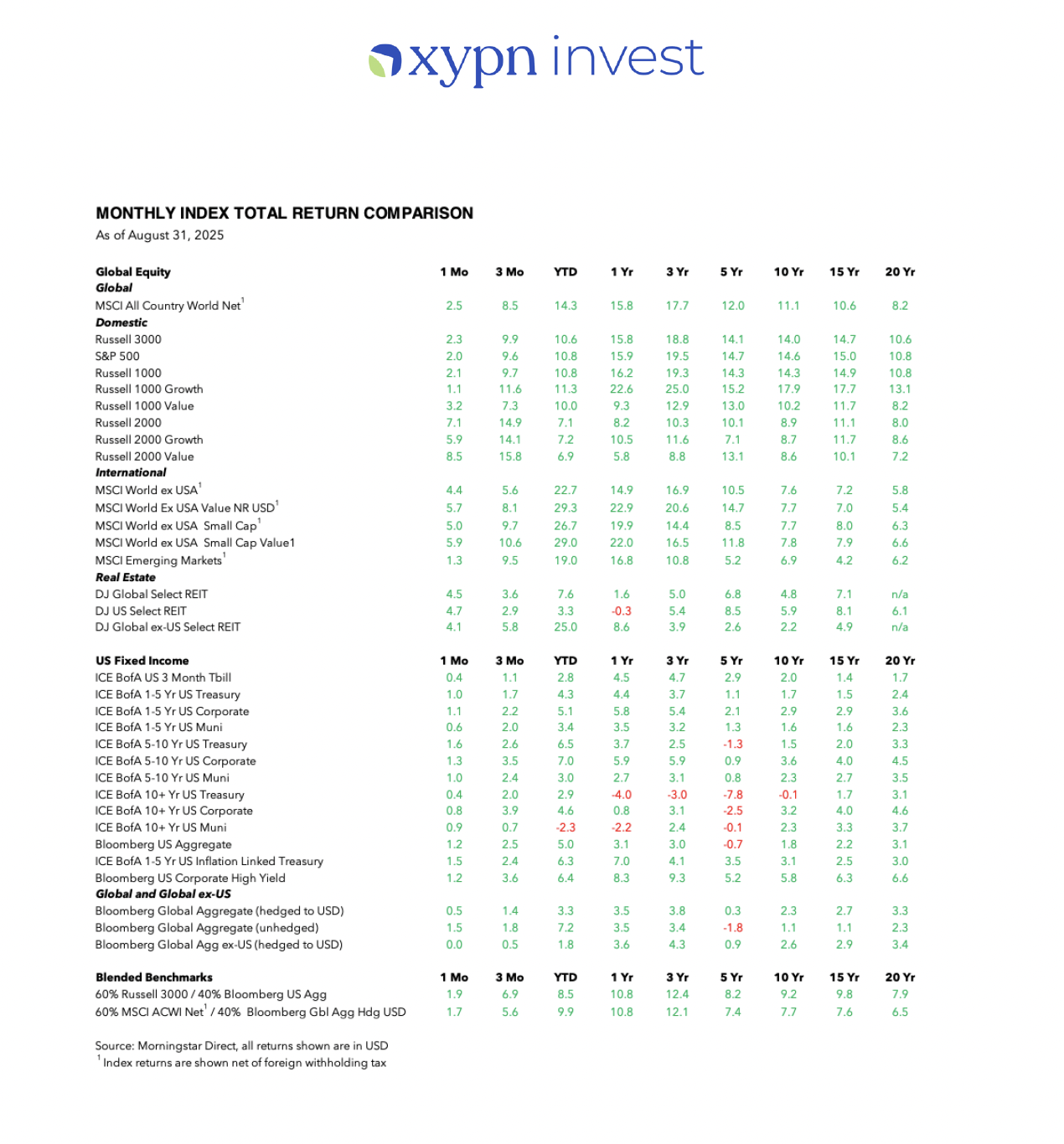

August 2025 Index Returns

In stocks (equities):

- August marks the fourth consecutive month this year in which the S&P 500 index (+2.0% in August) set a record high and is the first time the index broke the 6,500-point threshold.

- The U.S. stock market continued its upward trajectory (+2.3% in August, Russell 3000 index) fueled by stronger-than-expected corporate earnings reports, continued faith in the transformative effects of AI for company productivity and profitability, and a strong bet that the Fed will resume cutting interest rates in September. The leading asset class among U.S. stocks in August was small-cap value stocks (+8.5%, Russell 2000 Value index) as well as during the last three months (+15.8%), though it is the lowest performer (+6.9%) on a YTD basis.

- International developed stock markets as measured by the MSCI World ex USA index ended the month in positive territory (+4.4%) and continues to be aided in part by a falling U.S. dollar. Similar to the U.S., the best performing asset class last month within developed ex-U.S. stocks was small-cap value stocks (+5.9%, MSCI World ex USA Small Cap Value index), which have now posted a +29.0% gain so far on the year. Emerging markets stocks as measured by the MSCI Emerging Markets index were up +1.3% last month and are now up +19.0% on the year.

- On a YTD basis, the highest performing stock benchmark was international large-cap value, which gained +29.3% (MSCI World ex USA Value NR USD) and has outpaced U.S. large-cap growth stocks (Russell 1000 Growth index) by +18.0% so far.

In fixed income (bonds):

- Federal Reserve Chair Jerome Powell gave a speech last month at the annual Jackson Hole Economic Policy Symposium in which he hinted at a potential shift in the risks between the labor market and inflation now favoring a reduction in the Federal Funds rate. A lowering of the Federal Funds rate, which the Fed controls, would lead to a lowering of yields in ultrashort maturity treasuries but will not directly influence treasuries of longer maturities (e.g., 10-year treasury yields).

- Bond returns in Treasuries were positive for all maturities this month as yields fell across most of the yield curve with market participants ending the month expecting up to two interest rates cut by the Federal Reserve in its last three meetings between now and year's end according to CME FedWatch.

- Corporate and municipal bonds were positive across all maturity segments. The Bloomberg U.S. Aggregate Bond Index was up +1.2% last month.

- Outside of the U.S., the Bloomberg Global Agg ex-US (hedged to USD) Index was flat last month.

- All bond segments continued to show positive performance over the trailing one and three year periods with the exception of long-dated municipals and treasuries.

Even with continued volatility in the U.S. stock market and heightened geopolitical uncertainty around the world, a globally balanced 60/40 portfolio is now up +9.9% YTD, which reinforces the benefits of a well-diversified portfolio and that we must focus only on what we can control.

- As always, please let us know if you have any questions by emailing support@xyinvestmentsolutions.com

- As an additional note, please keep in mind that these reflect historical performance of the current models, not necessarily how accounts were invested in the past.