October 2025 Index Returns

In stocks (equities):

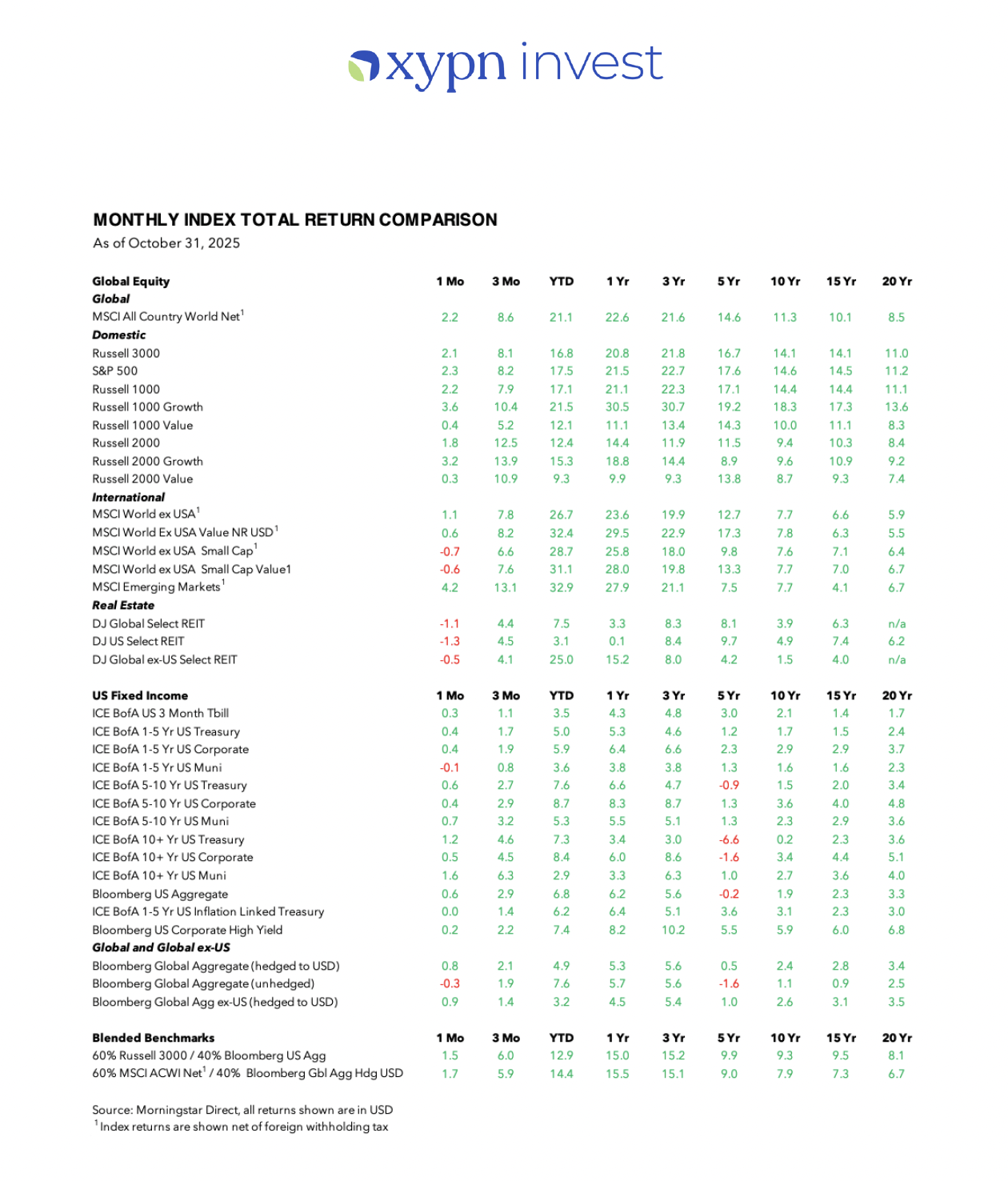

- Emerging markets stocks as measured by the MSCI Emerging Markets index were up +4.2% last month and +32.9% YTD, both the highest among all stock asset classes we follow. By comparison, the S&P 500 index returned +2.3% last month and is up +17.5% on the year.

- The U.S. stock market continued its ascent (+2.1% in October, Russell 3000 index) with the leading asset class among U.S. stocks in October being large-cap growth stocks (+3.6%, Russell 1000 Growth index).

- International developed stock markets as measured by the MSCI World ex USA index gained during the month (+1.1%) despite the U.S. dollar appreciating slightly. International developed small cap (-0.7%) and international developed small cap value (-0.6%) fell slightly during October but are still up +28.7% and +31.1% respectively on a YTD basis.

- Global stocks as represented by the MSCI ACWI have gained 21.1% YTD.

In fixed income (bonds):

- The Federal Reserve's rate setting body, the Federal Open Market Committee (FOMC), lowered the Federal Funds rate by 0.25% for the second time this year in their October meeting. A lowering of the Federal Funds rate, which the Fed controls, would lead to a lowering of yields in ultrashort maturity treasuries but will not directly influence treasuries of longer maturities (e.g., 10-year treasury yields). Fed Chair Jerome Powell made sure to note that another rate cut in December is not a foregone conclusion. As a result, market participants are now less certain about an additional cut taking place at the Fed's last meeting of the year in December, according to CME FedWatch.

- Bond returns in Treasuries were positive for all maturities last month as yields fell across most of the yield curve.

- Corporate and municipal bonds were positive across all maturity segments with the exception of short-term munis (-0.1%, ICE BofA 1-5 Yr US Muni). The Bloomberg U.S. Aggregate Bond Index was up +0.6% last month.

- Outside of the U.S., the Bloomberg Global Agg ex-US (hedged to USD) Index was up +0.8% last month.

- All bond segments continued to show positive performance over the trailing one- and three-year periods.

Despite ongoing swings in the U.S. stock market and elevated geopolitical risks worldwide, a globally balanced 60/40 portfolio has gained +14.4% year-to-date. This underscores the value of diversification and the importance of staying focused on the factors within our control.

- As always, please let us know if you have any questions by emailing support@xyinvestmentsolutions.com

- As an additional note, please keep in mind that these reflect historical performance of the current models, not necessarily how accounts were invested in the past.